The corporate net zero movement has a problem: it’s asking companies to commit to a goal they can’t achieve. The issue is not lack of intent or even resources. Rather, there is an inherent but subtle contradiction at the heart of net zero targets as they are currently understood. Consequently, even as more companies than ever have signed on to science-based targets (SBTs) for corporate-level decarbonization, some of the most ambitious, experienced, and well-funded corporate net zero programs are no longer compliant with established standards.

For example, this past spring, 3,482 companies were recognized as having adopted SBTs, up from fewer than 1,000 in 2021. But more than 200 companies were removed from the official roll call of companies committed to net zero this year, among them Microsoft, Amazon, and Walmart.

These companies have long been leaders in voluntary corporate action. Microsoft has pledged to be “carbon negative” and is investing heavily in zero-emission electricity. Walmart has mobilized one of the world’s largest and most complex supply chains to eliminate over one billion tons of upstream emissions. How can businesses with the most experience, the most resources, and the most progress end up offside?

Simply put, how companies are mandated to identify, calculate, and abate their carbon is fundamentally at odds with the sources of the emissions that, as a practical matter, they must find ways to abate. Ironically, this decarbonization dissonance has become disqualifying for climate leaders precisely because they have been working so diligently for so long: only by making the attempt in earnest has it become clear that net zero, as currently defined, is unattainable. And as other companies grapple with net zero targets and these hidden, inherent contradictions are revealed in high relief, some may choose a different path to eliminating emissions; but the very real danger is that a common response will be abandonment, something the voluntary climate movement can ill afford.

Thankfully, the net zero movement can be saved from itself. This paper argues that by using a novel combination of established carbon measurement methods and proven carbon market instruments, we can enable any company of any size, with any degree of climate ambition, to create business value for itself and advance its own decarbonization by driving the global economy’s transition to net zero.

This requires shifting mindsets surrounding three assumptions to enable a new focus on high-impact projects that decarbonize industrial production. Shift #1: from “think global, act local” to “think local, act global.” Shift #2: from “clean up your own mess” to “clean up the shared mess.” And shift #3: we need to unburden ourselves of the impractical “corporate net zero” target and embrace the surprisingly more reasonable ultimate goal of “global net zero.”

The alternative approach proposed by this paper can literally save the world. Indeed, conservative assumptions of the participation rate (percentage of industry revenue accounted for by participating companies) and participation level (percentage of revenue contributed by those companies) yield total subsidies that, when aggregated and appropriately focused, could ignite the radical decarbonization of sectors generating more than 90 per cent of total industrial emissions.

To understand the way forward, it will be helpful to understand how the established net zero framework has gone from a driver of positive action to an impediment to progress.

Three scopes and you’re out

A company’s carbon inventory comprises three “scopes.” Emissions from owned or controlled assets, such as the natural gas used to heat an owned office building, fall into scope 1. Scope 2 covers emissions tied to purchased energy (mostly electricity), while scope 3 captures emissions from the production of goods and services that a company purchases.[1]

To meet the established net zero standard, companies need to take direct responsibility for abating scopes 1 and 2 while working with suppliers to address scope 3. The specific inputs required by individual businesses vary dramatically across industries: legal, medical, financial, and hospitality services, for example, buy very different things. But the structures of carbon inventories in these sectors, along with the 300 other industries that collectively generate 85 per cent of global GDP (and only 9 per cent of emissions), are astonishingly similar: scopes 1 and 2 are usually less than 20 per cent of the total, and scope 3 is the rest.

Scope 1 emissions—typically less than 10 per cent of a company’s greenhouse gas (GHG) liability—are relatively easy to identify and abate. Many companies, for example, can find an environmental and economic case for scope 1 decarbonization through the electrification of vehicles and office heating and cooling systems. Scope 2 emissions are typically even easier to measure because energy purchases are recorded by utility bills.

Scope 3 emissions are where the existing approach to net zero falls apart because addressing them requires companies to ensure that suppliers responsible for two-thirds of their scope 3 inventory are also following the established net zero framework. (Why not 100 per cent? Standard setters recognize that, as a practical matter, it would be impossible for a focal company to convince every member of its supply chain to seek net zero accreditation.)

Suppliers’ electricity consumption is almost always the biggest driver of a company’s scope 3 inventory, at anywhere from 10 per cent to 30 per cent. The next five to ten inputs are typically idiosyncratic to each industry, but collectively they rarely capture more than another 20 to 30 per cent. From there, scope 3 becomes a long-tail problem of the first order, with each additional input accounting for one per cent or less of the total inventory. Consequently, capturing two-thirds of scope 3 can easily require 20 to 40 or more commodities (and likely hundreds of suppliers). A full accounting runs into hundreds of commodities and thousands of suppliers.

Consider a law firm. Its carbon footprint will be very likely about 2 per cent scope 1 (mostly from HVAC expenses that can be addressed with heat pumps) and 8 per cent scope 2 (electricity), with the remaining 90 per cent of its carbon inventory falling into scope 3. A qualifying SBT requires that the firm get suppliers generating two-thirds of this 90 per cent to sign up to their own SBTs.

A salient contributor to a law firm’s scope 3 is courier services, and courier services are about 60 per cent scope 1 (usually from the fuel burned in their trucks). Should a courier service supplier adopt SBTs, it might attack scope 1 emissions by electrifying its fleet. That’s a big lift, and the company might want its law firm customer to support that investment. But that law firm might account for, let’s say, 5 per cent of the courier’s total business, and so whatever support the law firm might provide is unlikely to make the necessary investment financially viable. Unless enough of the courier company’s customers make a similar commitment, the necessary shift is unlikely to happen quickly, if at all.

The courier also has its own scope 3 inventory to address. Couriers purchase trucks, and because the truck maker’s emissions are the courier’s scope 3, and therefore the law firm’s scope 3 as well, the truck maker also has to adopt SBTs. The truck maker, in turn, must abate its scope 1 emissions and get its own suppliers to follow suit.

This daisy-chain of contingent commitments is not a bug—it’s the explicit intent behind the design of carbon accounting and net zero targets. The existing theory of change is that through these concatenated covenants to decarbonize, the impetus provided by law firms will flow upstream and eventually eliminate the coal burned to make steel for the trucks, along with the bunker oil burned to ship iron ore to the steel foundry, and everything else besides.

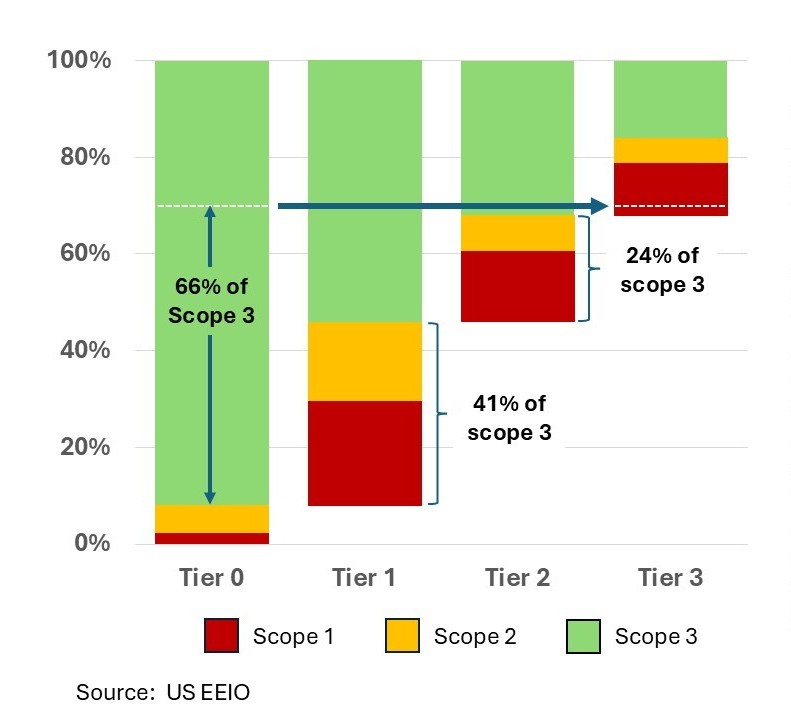

Figure 1 illustrates the challenge our law firm faces when initiating this cascade. Like most other companies with a very high proportion of total emissions lying in scope 3, it has a tier 1 supply base that is also dominated by scope 3. Consequently, while initial supplier conversations might go smoothly enough to get the requisite number signed on, the collision with expensive-to-abate upstream scope 1 is inevitable. And when enough of the supply chain hits insurmountable economic challenges, the net zero tapestry unravels. That’s a best-case scenario: in practice, net zero goals can founder simply because not enough tier 1 suppliers sign on to begin with.

Figure 1: Swimming upstream to find scope 3 emissions

Tier 0 captures the focal company’s carbon inventory. This illustration is for a typical law firm. Each tier can most readily address its scope 1 and scope 2 emissions. For the law firm, this Is only 8% of its total emissions. A Science Based (net zero) Target requires that the law firm secure commitments from suppliers generating 2/3 of its scope 3 emissions. The Tier 1 supply chain’s emissions are 41% scopes 1 and 2, which, coincidentally, accounts for 41% of the law firm’s scope 3. Tier 2 is also, coincidentally, 41% scopes 1 and 2, accounting for another 24% of the law firm’s scope 3. To reach the required 66% total, the law firm requires complete transparency into the third tier of its supply chain, which will comprise hundreds of commodities and tens of thousands of suppliers around the world.

Cost, complexity, impact

As we just noted, a law firm might be SBT-compliant on preliminary commitments from its suppliers, and then end up decertified because too many links in the needed chain of supplier net zero commitments break. The implication is that there is no deep difference between companies that are currently onside and those recently “de-committed.” Rather, companies like Microsoft and Walmart have been pursuing net zero long enough and vigorously enough to discover what others have yet to realize: that scope 3 is the kryptonite of net zero ambitions.

The problems begin with the complexity of the required supplier engagement. A law firm typically draws on more than 120 first-tier inputs. In addition to couriers, there are financial services, hotels, restaurants, other law firms, and so on. Each input is likely provided by more than one vendor, and many more in some cases, so reaching the requisite two-thirds of scope 3 emissions might easily involve getting several hundred companies to sign on. But each input has its own supply chain, with, on average, about 165 inputs—with most, if not all, provided by multiple vendors. In total, there could be half a million possible connections involved.

Worse, this complexity is dynamic: multiple supply chain tiers providing hundreds of inputs from thousands of companies, all constantly changing in ways that are difficult to monitor, if not invisible. Whatever mountains one might move to map one’s supply chain, the only safe bet is that it will have to be done all over again next year. Mapping and re-mapping the supply chain is not cheap, much to the delight of consultants claiming to be able to do this. And that expense is in addition to the spending required to address carbon-intensive processes, which tends to increase as you move upstream.

Speaking of expenses, recall that this is voluntary climate action, and so success depends entirely on companies’ willingness to pay. Beyond a few high-profile and often tech-driven organizations (Meta, Amazon et al.), anecdotal evidence suggests very few companies are willing to spend much more than 0.01 per cent to 0.05 per cent of annual revenue, even for just a few consecutive years.

Unfortunately, this level of spending is likely less than a tenth of even a minimum requirement. For example, the cost per ton of carbon abated for high-emitting, high-intensity inputs can range from negative (carbon free can be cheaper) to several hundred dollars per ton for especially hard-to-abate inputs, such as steel or trans-oceanic shipping. The 64th-largest U.S. law firm has US$1 billion in revenue and an implied carbon footprint of 44,000 metric tons. Just finding all that carbon could cost US$1 million to US$3 million—already more than most companies seem willing to spend in total. The cost of abatement could easily run US$10 million or more, or 0.1 per cent of revenue and up.

Part of what makes it difficult to invest is that the value to the focal company can be difficult to determine. Absent carbon prices, there is little direct financial incentive to decarbonize. Consequently, voluntary investments, especially in supplier decarbonization, are typically justified as brand equity initiatives—which need broad appeal and the ability to withstand scrutiny. This requires squeezing between the Scylla of those who decry the entire net zero effort as a misguided concession to “woke” interests and the Charybdis of those who value decarbonization but are deeply suspicious of corporate greenwashing. With credibility relying on delicately balanced claims tied to a company’s detailed understanding of its complex, dynamic global supply chain, the entire house of cards can collapse the second anyone suggests the complex web of assertions being made is in any way suspect.

Finally, consider the potential climate impact. Each company’s individual contributions must demonstrably accelerate the decarbonization of economic activity, or there is no point. But making a meaningful contribution is too often proving a fool’s errand: what can a few million dollars do to move the needle on the production of hundreds of billions of dollars of production of a globally sourced commodity?

A complex, dynamic supply chain that can’t really be traced; an expense that overwhelms the demonstrated appetite to spend; a nebulous value proposition; and a questionable connection to meaningful impact. Hardly a recipe for success.

Hidden in plain sight

The current approach to global net zero assumes that if each company sets and meets its own goals for decarbonization, the result will be economy-wide decarbonization. The bumper sticker slogan for this theory of change is well known: think global, act local.

Scope-based accounting translates that aphorism into action. Specifically, scope 1 makes a company accountable for its own emissions, while scope 3 creates accountability for the emissions generated at its behest. In this way, a company’s climate ambition reaches beyond its organizational boundaries into the larger ecosystem of companies in which it is embedded. In other words, isolated corporate decarbonization efforts are expected to drive systemic transformation by setting off an interlocking series of reduction efforts and knock-on net zero commitments that eventually touch every corner of the global economy.

“Thankfully, the answer does not lie in looking harder, but instead in allowing ourselves to see clearly what is already in full view.””

As a practical matter, “acting local” has led companies to begin their efforts with measurement and prioritization. This follows a powerful problem-solving heuristic that has proven highly effective in many other circumstances. After all, if you want to cut costs, it isn’t unreasonable to start by determining what and where they are and then focus reduction efforts on the largest cost drivers.

The belief that “you can’t manage what you can’t measure” often proves effective when dealing with scope 1 and scope 2 emissions. But measuring scope 3 with the seemingly requisite accuracy has proven elusive. This shouldn’t surprise anyone: supply chain executives have wanted greater upstream transparency for decades for reasons having nothing to do with carbon emissions. That’s why it is difficult to see how the necessary supply chain transparency can now be achieved simply because of the additional motivation of reaching net zero. As a result, “you can’t manage what you can’t measure” runs headlong into “you can’t measure what you can’t find.”

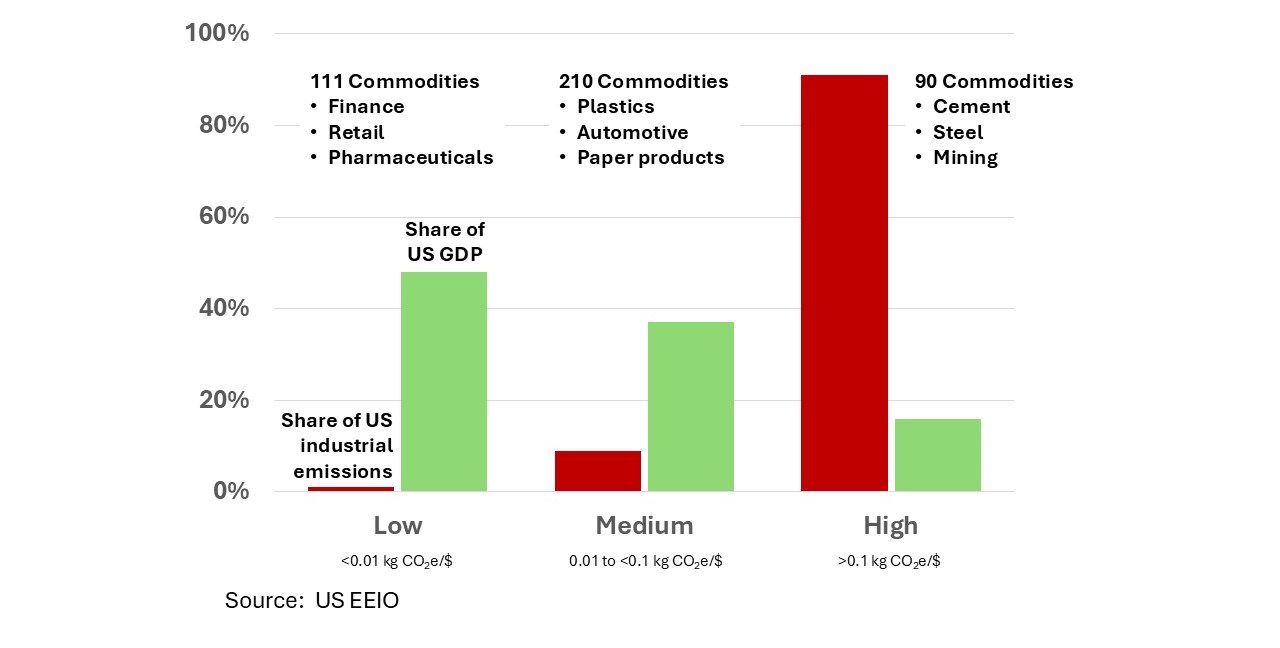

Thankfully, the answer does not lie in looking harder, but instead in allowing ourselves to see clearly what is already in full view. According to the U.S. economy’s official GHG inventory, based on U.S. Environmental Protection Agency (EPA) estimates, almost all U.S. industrial carbon emissions come from the production of a relatively small number of commodities (which collectively produce relatively little economic wealth). Specifically, as seen in Figure 2, of the 411 outputs that capture the full scale and scope of U.S. economic might, 90 high-intensity, hard-to-abate (HTA) commodities emit more than 91 per cent of total GHG emissions while generating a mere 15 per cent of total GDP.

Figure 2: Money on the left, emissions on the right

What does this mean for net zero? It means that instead of fruitlessly trying to untie the Gordian Knot of scope 3 emissions, we can cut it. Companies seeking to figure out where most of their carbon comes from don’t really need to embark on a multi-million-dollar, multi-year death march up their supply chain because, no matter the business, we know 90 per cent or more of all emissions are generated by agricultural products, construction materials, transport, mining, chemicals and plastics, and so on. We know this simply because that’s where 90 per cent of all emissions in the economy come from.

By way of analogy, imagine you live in a watershed sustained by glaciers. You want to know where the water comes from. You could try tracing the streams and rivulets by which the water trickles down the slopes. But those waterways are complex, and it is hard work trekking up the mountainside to follow them upstream. Worse, if you can’t find the source before winter, you’ll have to start all over again next spring, because many of those waterways change constantly. You might work for years and never find the source. Or you could just point to the glaciers.

Cleaning up the collective mess

The established net zero standard requires companies to take direct responsibility for their own mess (scopes 1 and 2) while encouraging suppliers to do the same. But while “clean up your own mess” sounds fair, it really isn’t, because companies with more carbon-intensive production processes often find abatement far more challenging and expensive. They can only make the necessary investments if their customers are willing to pay the requisite green premiums.

As shown in Figure 3, however, it turns out that most commodities do most of their business with commodities of similar carbon intensity. That is, the value creation process generally begins with raw material extraction, which eddies in the whirlpools of the high-intensity sectors before spilling over into the medium-intensity sectors, where it lingers before doing the same in the low-intensity realm, until terminating in final use and a dollar of GDP.

Consequently, high-carbon companies find themselves both beseeching and being beseeched for big-dollar support for decarbonization. When you, your customers, and your suppliers all have your hands out at the same time, and you are all relatively small-dollar, thin-margin producers, no one gets much of anything.

Similarly, low-intensity commodities, like banking and lawyering, do most of their business with each other, while enjoying much greater revenue and proportionate value added. Yet, because their economic connection to the upstream carbon is highly attenuated and diffuse, there is no ready mechanism to connect any willingness to pay on their part with the upstream sources of carbon.

Figure 3: Money flows within intensity categories, not across them

For low-intensity companies to make rational investments in decarbonizing upstream production, we need some way to tell our law firm how much of which of those high-intensity commodities is driving its inventory. This can be done with the help of the U.S. Bureau of Economic Analysis (BEA), which tracks business payments for inputs required to produce a given output.

Aggregating across the total production of each commodity and the total expenditure on all inputs yields a 411 × 411 direct requirements (DR) matrix: the average dollar value of each input required to produce one dollar of each output. This synthesis reveals that law firms purchase, on average, 1/100,000th of a cent of fertilizer for each dollar of services they sell. Predictably, that’s not much (the only surprise is that it’s not zero!). But law firms spend two cents on financial services for each dollar of revenue, reflecting an intuitively much higher direct reliance on banks than on fertilizer.

Using computationally straightforward matrix algebra, the BEA then infers the total requirements (TR) of each commodity for every other commodity. Now we know law firms have a total requirement for fertilizer of 0.02 cents per dollar, about 20,000 times more than their direct requirement. That figure captures exactly what we want: the total amount of fertilizer required by every stage of every value chain that feeds every input required to provide legal services.

By combining the EPA’s direct emission (scope 1) factors for every commodity with the BEA’s data on the required inputs to produce each commodity, one can generate a sound carbon allocation that usefully captures a company’s scope 3 carbon burden.

In a matter of minutes, this allows a company to use its existing GHG Protocol-compliant carbon inventory—the same one that leads to a futile, soul-crushing exercise in scope 3 measurement—to create an accurate-enough estimate of the sources and quantities of all the upstream scope 1. The total carbon burden will remain identical (not as a happy coincidence but as a mathematical necessity) and now we know how much a company relies on which upstream HTA inputs. This allows companies to calibrate their contributions to the magnitude of their reliance on specific commodities, regardless of their actual purchasing behaviour.

For example, rare is the law firm that buys barrels of hydrogen peroxide, yet every dollar of legal services relies on 0.2 cents of the stuff. Its manufacture is so carbon intensive that it is, along with other organic chemicals, the fourth-largest contributor to a law firm’s total footprint (about 3.5 per cent). Armed with this knowledge, a law firm might wish to support zero carbon hydrogen peroxide production as part of its scope 3 reduction strategy.

Unfortunately, there is extreme physical and economic separation between lawyers and chemical reactor vessels. And so, while lawyers might gladly pay to decarbonize the production of this commodity, there is no way for them to do so.

Except maybe there is. Connecting those willing to buy “green” commodities but unable to source them with those who want to produce green commodities but can’t sell them has been solved once already—for electricity.

As much as 30 years ago, when renewable electricity generation was technically feasible but economically impractical, some companies were willing to pay for green electricity, but unable to do so because the grids they were on had little or no renewable generation capacity. At the same time, there were would-be producers of green electricity who lacked sufficient demand on the grids they fed into. Instruments that evolved to become what are today known as virtual power purchase agreements (VPPAs) were created to enable companies on “dirty grids” to pay for green electricity they did not consume. In return, they got a renewable electricity certificate (REC) that allowed them to claim a reduction in their scope 2 emissions.

There were teething pains and criticisms to overcome.[2] Nevertheless, VPPAs and RECs allowed the dispersed and fragmented demand for green electricity to be aggregated and focused on specific projects that decarbonized electricity production. Each participating company was able to calibrate its investment to its use of electricity, and the resulting incremental demand proved critical in the earliest days of solar and wind deployments, when small absolute increases delivered disproportionate reductions in cost. This solution is a specific example of an “inset” coupled with “book-and-claim” recognition.

This approach has been recognized by standard setters as a valid way to abate scope 2 emissions, and it’s an approach with general application. Keep in mind that there are ways to manufacture near-zero carbon concrete, steel, and ammonia for fertilizer, among other HTA commodities. It is also possible to identify and quantify how much of each of these commodities any given company relies upon, in expectation, using the method described above. Companies wishing to reduce their supply chain emissions arising from their reliance on inputs they don’t purchase directly can purchase the environmental attributes of green versions of those inputs and claim an environmental attribute certificate (EAC). The difference between the emissions documented in the EAC and the imputed emissions associated with higher carbon production deemed to be in the purchaser’s inventory is captured by a virtual commodity inset (VCI). The company can “book” its purchase of the EAC on a credible registry and “claim” the associated scope 3 reductions by retiring the VCI on the same registry.

For example, we know that approximately 8 per cent of a pharmaceutical company’s scope 3 emissions are generated by grain farming.[3] To address that burden, a drug company with, say, US$10 billion in revenue can infer that there are so many tons of carbon in its inventory from the production of a given quantity of grain. It could then purchase EACs attached to low carbon production of the relevant quantity, thereby generating a VCI. When aggregated with the EAC purchases of other companies that also have a specifiable reliance on grain production, the resulting focused revenue subsidy could allow a farm employing, say, regenerative agriculture practices, to produce that much more decarbonized commodity. This displaces dirty production and advances the adoption of sustainable practices, all without a direct value chain linkage between the grain being subsidized and the grain inputs used, however indirectly, by the companies providing the subsidies.

Some people get nervous about separating purchase and use, worried that insets will end up no better than “offsets,” a companion construct that has been the subject of severe criticism. Offsets tend to focus on avoided emissions or carbon removal entirely independently of any value chain connection, e.g., preserving forests or subsidizing low-carbon cookstoves in rural areas. It can be difficult to ensure appropriate “additionality,” that is, establishing that a given initiative would not have happened without the intervention. “Leakage” is also often a problem: an offset purchaser, for example, could pay to protect a specific forested area from logging, but by removing that supply from the market, another plot of land is cut down in its stead. Finally, there is a question of “permanence.” Protected forests might be destroyed by fire or disease, so carbon emissions might only get delayed, or promised planting might not get done at all.

These concerns are legitimate, but insets need not succumb to these offset failings. To make insets work, we just need to abandon the assumption that corporate net zero is the goal and start thinking about global net zero instead.

From local to global

Many companies claim they are on track to achieve net zero status, some as early as 2030. This can appear fantastically ambitious when one contemplates carefully that every corporate inventory comprises emissions from an untraceable global supply chain of hard-to-abate (read “expensive”-to-abate) commodities. Nobody can ensure that all the right suppliers are making the requisite commitments—recall, it was this very challenge that derailed the SBT commitments of more than 200 companies, some of which had among the most sophisticated and advanced scope 3 initiatives.

“In voluntary markets, the opportunity is to focus what little money is available on small-scale, broad-scope projects that demonstrate the viability of system-level transformation.””

The inset solution described above opens the door to achieving corporate-specific net zero status. But purchasing the requisite insets in the necessary quantities is likely prohibitively expensive, and easily 0.1 per cent of revenue or more—a princely sum for a voluntary expense. And if one can’t afford the EACs to reach net zero by proxy, then no one can be sure that the relevant inputs are truly decarbonized until, in essence, all the production of that commodity is decarbonized.

In other words, no one will be net zero until everyone is net zero. Consequently, even if the voluntary market reorients around “think local, act global” and “clean up the shared mess,” there still appears to be no path to success. But while individual companies can’t achieve corporate net zero, they can still meaningfully contribute to global net zero. The key is abandoning the futile quest to zero-out one’s own inventory and instead seek to accelerate the transformation of specific high-emitting sectors.

To be clear: there is no substitute for the gigaton-level elimination of emissions, globally and rapidly. But that objective is best addressed at the policy level through carbon taxes, emissions caps, and the like. In voluntary markets, the opportunity is to focus what little money is available on small-scale, broad-scope projects that demonstrate the viability of system-level transformation.

A template for voluntary action

Since its founding in 2003, Tesla has received material government support in the form of loans and convertible equity, all of which it has repaid. As critical as this assistance was, however, the cash needed to create a new car company exceeded what both government and private capital were willing to fund. Until costs came down and volumes went up, Tesla needed ongoing revenue subsidies.

That support came in the form of the California Zero-Emission Vehicle (ZEV) tax credit scheme. Introduced in 1990, this law compelled automakers operating in the Golden State (and several adjacent markets) to either manufacture zero-emission vehicles or purchase credits from automakers with surplus zero-emission production.

For years, automakers proved unable to meet the law’s requirements because there was no significant zero-emission production, and so these mandates were repeatedly dialed back in response to automaker intransigence. Then Tesla appeared. Incumbents could no longer claim electric vehicles (EVs) were “impossible” or that they were unable to purchase the requisite credits. And because Tesla didn’t make internal combustion engine (ICE) cars, it was able to reap a revenue subsidy from other automakers of up to US$3,000 for each car it sold.

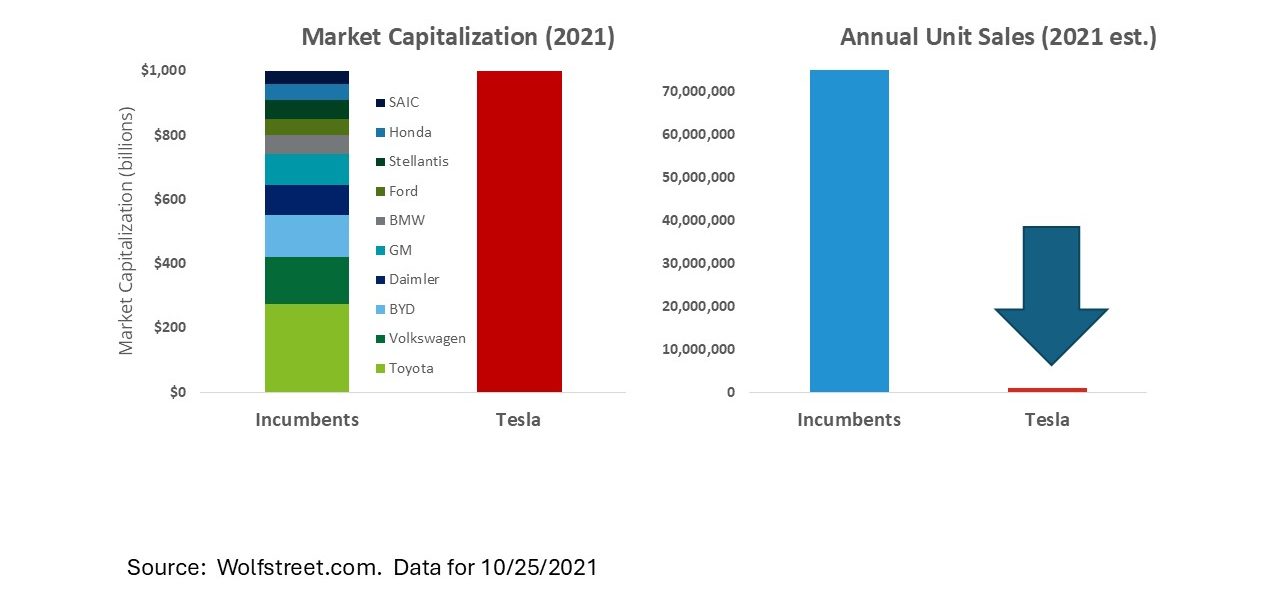

Through 2020, Tesla received more than US$6 billion in such subsidies, which allowed it to refine its reinvention of the automotive supply chain and production processes. By 2021, Tesla’s business had found its footing. Its cars were popular while costs were competitive and declining. Its prospects were sufficiently bright that its market value was equal to that of the next ten largest automakers combined. Its success inspired other EV companies, many of them Chinese. In short, Tesla subsidies provided “activation energy” for a structurally cheaper and radically decarbonized approach to personal vehicle transport. And as seen in Figure 4, Tesla changed the industry despite very low global market share.

Figure 4: Markets anticipate industry transformation

Like renewable power generation, subsidies are playing an ever less critical role in driving EV adoption. EVs are not just zero emissions, they are rapidly becoming cheaper to manufacture and operate, not to mention better suited to large-scale recycling. Meanwhile, although the fate of Tesla remains highly relevant to the U.S.-based production of EVs, it is likely that the global shift to electrified transport is inevitable, as seen in Figure 5.

Figure 5: EVs are the future of passenger vehicles

So, what’s the lesson? Let’s risk an overstatement (but only mildly) and say California managed to transform the global passenger vehicle market with just US$6 billion in subsidies paid to a market innovator by industry laggards. It pushed the snowball off the mountain, enabling market forces to create an avalanche.

Tesla’s support came from a compliance carbon market, that is, from obligatory participation. The relevant lesson, however, is not what motivated the subsidies, but how they were deployed: aggregated and focused on a transformational set of technologies and processes.

Look at steel. Refining iron ore typically relies on reacting iron oxides with carbon monoxide to leave behind pure iron with CO2 as a byproduct. But one can instead create direct reduced iron (DRI) by reacting the oxide with hydrogen generated by electrolyzing water with electricity from renewable sources. This leaves behind pure iron with water as a byproduct.

When incorporated into existing productions systems, this radically lower-carbon alternative for steel production implies a structurally higher cost. But system change via re-imagining the entire value chain can make it economically attractive. For example, instead of shipping raw ore to refining locations, refining infrastructure could be located at the mine. The cost and emissions from transportation would fall by orders of magnitude, and that’s in addition to the reduction in emissions from production.

Similar decarbonization opportunities exist for other HTA inputs (concrete, ammonia, mining, and so on). But creating radical system-level solutions is not something incumbents or capital markets are consistently able to do because there is no mechanism that allows companies or investors to capture the value of decarbonization efforts quickly or reliably enough.[4] But through EACs and VCIs, enabled and accounted for via book-and-claim platforms, voluntary market support can be aggregated and focused on “lighthouse projects” that demonstrate the viability of smaller-scale but broad-scope system-level solutions. This would reduce risk for private investment and increase capital deployed, while shortening the time to both cost competitiveness and growth to global scale.

There are likely to be only a few qualifying projects for each commodity, and in each case the support needed will likely be relatively low, maybe a few million dollars annually. And this is not perpetual corporate charity, but a relatively short commitment—perhaps five years. Keep in mind that, like Tesla, makers of low-carbon commodities need not reach scale on the back of their initial enabling subsidies; rather, their support need only create a credible line of sight to cost competitiveness, at which point private capital can then rush in and drive industry transformation.

The marketing value of such support to purchasers of EACs will then be tied to driving industry transformation, not merely achieving their own corporate net zero. That shifts the value proposition from total tons abated or cost per ton of carbon to demonstrations of the possible and the implications of innovation on global emissions. In this world, being among the first to support a lower-carbon alternative is likely to carry the greatest return. Consequently, participating companies will be more motivated to seek out projects that have yet to attract much support. In other words, there will be far less value in being the 50th company to support low-carbon concrete than in being the fifth to support low-carbon ammonia, even if the cost per ton is much higher and the total tons abated is much lower.

Some back-of-the-envelope estimates suggest that such support could be transformative for nearly the full range of high-intensity commodities. For example, assume companies generating only 25 per cent of revenue in the low- and medium-intensity industries sign on. In most cases, this means securing the participation of perhaps the largest four to ten organizations. Assume further that these climate leaders devote 0.02 per cent of their revenue to decarbonization support. This level of involvement, which hardly seems aggressive, translates into a 20 per cent annual revenue subsidy for 0.1 per cent of production of the full complement of high-intensity sectors. When one considers that Tesla’s transformation of the global auto sector was built on revenue subsidies of approximately 5 per cent and a market share of 0.3 per cent, this seems highly material.

Companies providing such subsidies, of course, must choose projects like educated investors. As a result, it will be incumbent upon participating companies to support solutions with the best chances of success. This might require some hard choices between scrappy start-ups and incumbents attempting to leverage an existing asset. But then, this solution’s merits are that it can work, not that it is easy or foolproof.

Dropping the curtain on corporate net zero

The first act for corporate climate action featured charitable contributions to high-profile nature-based solutions. The associated marketing material inevitably featured sylvan wilderness sheltering under well-intentioned charity. These efforts continue, and can be effective, but it has become clear that what some have referred to as “climate indulgences” are far from sufficient. And with limited voluntary funds to spare, ongoing challenges suggest that such efforts should be de-emphasized.

The promulgation of the corporate net zero construct was a significant advance, because it shifted the focus of companies from merely “doing good” to taking responsibility for their direct impact on the environment. The priority became the elimination of GHG emissions through the adoption of low- or zero-carbon technologies. There can be no doubt that without this reallocation of effort, corporate climate action would likely have remained largely performative.

But it’s time to drop the curtain on this second act because, as Microsoft and Walmart learned, while a company can make a good start on corporate net zero, it will never achieve that goal following the dominant net zero paradigm. Neither can the current focus on measurement, engagement with the direct supply chain, and maximizing the efficiency of abatement strategies deliver sector-level change. In contrast, a global net zero framework built on useful estimation, focused insets, and project-level price subsidies can get the job done by connecting voluntary corporate action with credible, high-impact results.

Under the framework proposed by this paper, companies can choose which commodities to support, and only need to participate up to the point that their willingness to spend permits. That support is aggregated and focused, in a manner similar to what has worked so well in electricity markets. And because the target is no longer corporate net zero, but driving global transformation, companies can calibrate their support to their assessments of the value received.

Deploying EACs and VCIs via book-and-claim obviates any physical connection between the company providing the support and the supported production. As a result, funding companies will likely be able to direct their support to projects that are relevant to the constituencies they wish to appeal to, perhaps based on the commodity in question and where it is produced.

For example, a global law firm headquartered in Toronto might choose to fund low-carbon agriculture in southwestern Ontario, appealing to its local market’s sensibilities, but also fund electrified lithium mining in Peru, to curry favor with globally minded law school recruits. A Vancouver-based movie studio could focus on radically decarbonized mining in British Columbia but net zero cattle ranching in Brazil based on a similar balancing of salience and impact.

Collectively, these considerations will allow the voluntary market to allocate capital efficiently to a succession of commodities, with each receiving support based on its decarbonization potential, and each graduating to subsidy-free, rapid scale-up as that potential crystallizes.

And that’s how corporations can decarbonize the world even though they cannot decarbonize themselves.

Corporate net zero is dead. Long live global net zero.

Footnotes

[1] Carbon emitted downstream in the use or disposal of a product also falls under scope 3. But few companies report downstream emissions and including them in this paper unnecessarily complicates the discussion.

[2] For example, the market learned to provide assurances that renewable capacity funded by VPPAs is additional, that is, the VPPA is a determining factor in its deployment. Mechanisms to ensure that the renewable capacity is truly displacing dirty generation have also required improvements.

[3] This surprises most people in the drug industry because they purchase essentially no grain directly, and typically do not in their second-tier supply chain, either.

[4] Direct customers of decarbonized versions of high-intensity, high-emitting industries typically face the same challenges themselves.

About Author

Michael E. Raynor is an Associate Professor at Ivey Business School and a co-founder of S3 Markets (www.s3markets.com), a platform that provides supply chain insets to companies pursuing voluntary climate action. He is the author or co-author of hundreds of articles and four bestselling and critically acclaimed books, including The Innovator’s Solution, co-authored with the late Clayton M. Christensen. Raynor has a doctorate from Harvard Business School. He lives in Mississauga. CONTACT: mraynor@ivey.ca